| What Is A Credit Score?

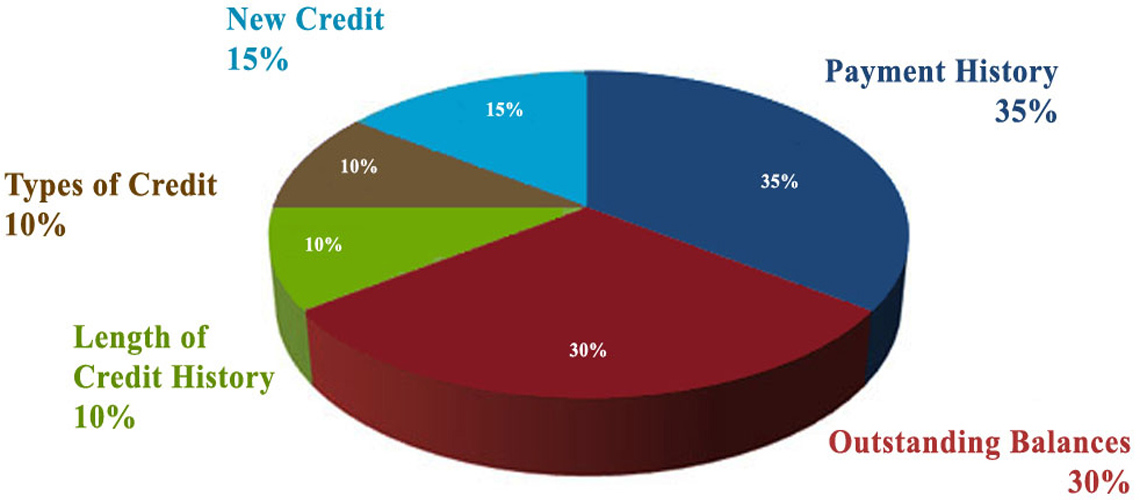

Lenders want their evaluation to be as accurate, objective and consistent as possible. To help achieve this goal, home mortgage lenders use credit scores to assist in the underwriting process. Credit scores are numerical values that rank individuals according to their credit history at a given point in time. A credit score is based on past payment history, the amount of available credit, and other factors. According to Fannie Mae and Freddie Mac, two large investors in mortgage loans, credit scores have proven to be very good predictors of whether a borrower will repay his or her loan. Keep in mind that even when a credit score is low, there are other factors that could be considered to overcome negative credit issues and satisfy other underwriting criteria. What is a FICO Score? “FICO” scores are a type of credit score developed by Fair Isaac & Company. FICO scores use credit bureau information to obtain a number that analyzes a history of using credit and how likely someone is to be a safe credit risk. FICO scores range from approximately 350 to 900. The higher the score, the lower the probability of default on a loan. How Can Credit Scores Affect the Price of the Loan? Just as credit scores are one factor in determining loan qualification, they may also be a factor in determining the price of the loan. The price of a loan means the interest rate and the points charged by the lender. The price charged for a loan will be higher or lower depending on various factors. Many home loans are sold to investors (usually called the secondary market), and investors will pay a more favorable price for loans they feel have a low risk of default. There are many other factors relating to an individual borrower’s situation that may also affect the price of a loan. These include the type of property secured by the loan, the amount of the borrower’s equity in the property (down payment), the value of the property compared to property values in the area, the lender’s cost to complete the loan and the type of loan selected. For example, the interest rate of a loan for which the borrower has made a 20% down payment may be lower than a loan for which the borrower has made a 5% down payment because the first borrower has more equity in the property and, thus, a greater incentive to make the payments of the loan. In layman’s terms you’ve got more skin in the game. |

When lenders evaluate a loan application, a process called underwriting, they evaluate your ability and willingness to repay the loan by reviewing the income and stability of past earnings. This practice helps the lender to determine if the borrower can afford the loan payments. The review of past credit history is used to judge the willingness of the borrower to repay the loan.

When lenders evaluate a loan application, a process called underwriting, they evaluate your ability and willingness to repay the loan by reviewing the income and stability of past earnings. This practice helps the lender to determine if the borrower can afford the loan payments. The review of past credit history is used to judge the willingness of the borrower to repay the loan.Additional Resources for Home Buyers

- A Heads Up for Home Buyers

- Being Prepared

- For First-Time Buyers

- How Can I Help You?

- Do You Need a Buyer Agent

- Getting Pre-Approved

- Buyers Frequently Asked Questions

- How Much Should I Offer?

- Offers and Purchase Agreements

- Who Pays for What?